Best Home Insurance for Homeowners: What Actually Makes a Policy Worth Paying For

Here’s something strange about home insurance right now. We’re all paying more for it than ever, with rates jumping nearly 47% across the country between 2020 and 2025, and yet millions of homeowners are still dangerously underprotected.

That combination should bother you. A bigger bill doesn’t automatically buy a better safety net.

I’ve watched too many people learn this the hard way, usually while standing in front of a damaged home holding a payout that doesn’t come close to covering the repairs. Let’s make sure that’s never your story.

This is a plain-English guide to finding the best home insurance for homeowners: what to look for, what to skip, and how to stop overpaying for coverage that won’t show up when you actually need it.

First, Let’s Be Honest About What “Best” Means

When people search for the best home insurance for homeowners, most are quietly thinking cheapest. I get it, the premium stings. But cheap and best are rarely the same thing.

The best policy is the one that fits your home, your risks, and your budget, and pays out fairly when disaster hits. A bargain price means nothing if the company fights you on every claim.

Think of it like a parachute. You don’t shop for the lightest, cheapest one. You shop for the one that opens.

What You’re Actually Paying For

A standard policy isn’t one product. It’s a bundle of separate protections, and most homeowners only ever picture one of them.

In the U.S., roughly 78% of homeowners carry an HO-3 policy, mostly because it covers a wide range of risks at a sensible price. Here’s what’s tucked inside it.

Your Home’s Structure

This is dwelling coverage, and it pays to rebuild the bones of your house: walls, roof, floors, and built-in systems. If a fire or storm levels the place, this funds the rebuild.

It’s also the single most common spot where people end up underinsured.

Everything Inside It

Personal property coverage handles your belongings: furniture, electronics, clothes, kitchenware. If they’re stolen or destroyed in a covered event, this helps replace them.

Watch the fine print, though. High-value items like jewelry, watches, or art usually have hard caps, so you may need a separate rider to fully protect them.

Protection From Lawsuits

Liability coverage steps in when someone gets hurt on your property or you’re blamed for damage to others. It covers their medical bills and your legal costs.

These claims are uncommon, around 2% of all claims, but they average roughly $30,000 each. That’s not a number you want to pay yourself.

A Place to Stay During Repairs

Loss of use coverage pays for hotels, meals, and rent if your home becomes unlivable after a covered disaster. Plenty of people don’t realize they have it until they’re suddenly living out of a suitcase.

How Much Does Home Insurance Cost in 2026?

Let’s talk money, since it’s usually the deciding factor.

The national average sits somewhere around $2,400 a year, but that average hides enormous swings. In Hawaii you might pay about $800, while in Oklahoma the average climbs north of $5,000.

Why Your Neighbor Pays a Different Price

Two nearly identical houses can carry very different premiums. Insurers weigh a long list of factors, including:

- Location and local weather or wildfire risk

- The age, size, and building materials of your home

- Your roof’s age and condition

- Your claims history (and sometimes the previous owner’s)

- Your credit history, in most states

Why Rates Keep Climbing

The jump in premiums isn’t random. Between 2020 and 2024, the U.S. averaged around 23 billion-dollar weather disasters a year, up sharply from previous years.

Add rising labor and material costs, and every repair gets pricier for insurers, who then pass that along to you. It’s frustrating, but understanding the why helps you shop smarter instead of just angrier.

5 Questions to Ask Before You Buy

Forget memorizing jargon. If you can answer these five questions honestly, you’ll already be ahead of most buyers.

1. Am I insured for what it costs to rebuild, or just what my house is worth?

This is the big one. Market value and rebuild cost are different numbers, and confusing them is how people end up short.

After the 2021 Marshall Fire in Colorado, a University of Colorado study found 74% of affected homeowners were underinsured, by an average of $139,000. Tie your dwelling limit to rebuild cost, and check it every year.

2. What’s specifically excluded?

Every policy lists what it won’t cover, and that list is where the painful surprises hide. The biggest gap: standard policies don’t cover flood damage.

And don’t assume you’re safe because you’re not near water. Roughly 80% of flood claims happen outside designated high-risk zones.

3. Can I actually afford this deductible?

A higher deductible lowers your premium, which looks great on paper. But it’s the amount you pay out of pocket before coverage kicks in.

Only raise it to a number you could cover tomorrow without losing sleep. Saving $15 a month isn’t worth a $5,000 bill you can’t pay.

4. How does this company handle claims?

A cheap policy is useless if the insurer stalls or denies you. Around 5 to 6% of home insurance claims get fully denied, so reputation matters.

Before you sign, check the company’s financial strength rating, read claims-satisfaction reviews, and ask neighbors about their real experiences.

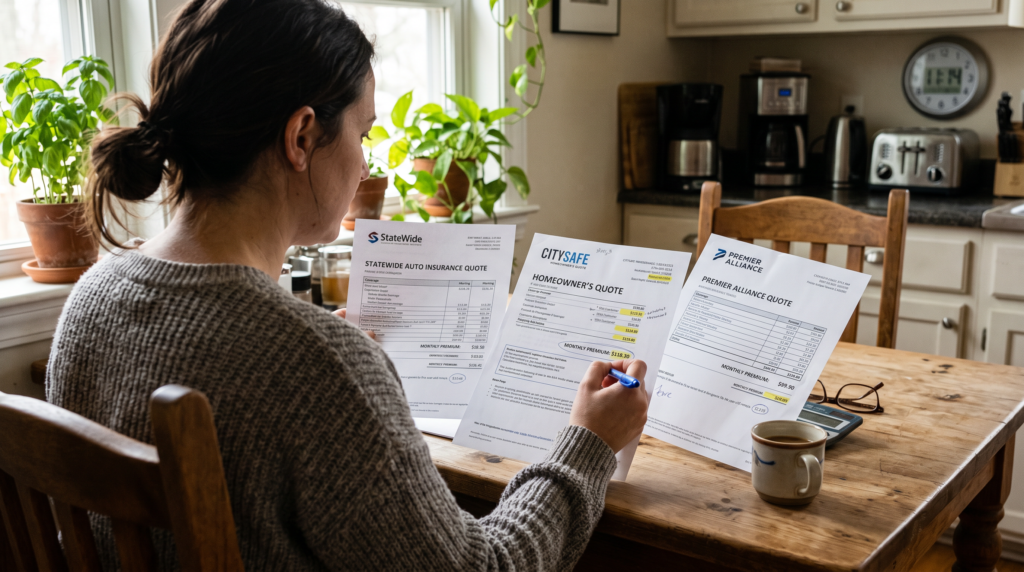

5. Am I comparing the same thing across quotes?

Never buy from the first company you call. Coverage and price vary wildly between insurers, even for the identical house.

Pull three or four quotes with matching limits and deductibles so you’re actually comparing apples to apples, not a stripped-down plan against a full one.

READ MORE The Best Solar Panels for Residential Homes (2026 Guide)

READ MORE How Long Do Solar Panels Last? Here’s the Honest Answer

The Mistakes That Cost Homeowners the Most

Some errors are minor. These ones can cost you your home, so they’re worth knowing.

A common pattern looks harmless at first. To shave the monthly bill, a homeowner quietly trims coverage, maybe bumping the deductible, dropping a flood rider, or cutting replacement cost protection. Each tweak feels reasonable in the moment.

Then a storm hits, the payout falls tens of thousands short, and a manageable monthly saving turns into a financial disaster. One Florida contractor described families ending up months behind on their mortgage after exactly this kind of trade-off.

Here are the slip-ups that do the most damage:

- Insuring for market value instead of rebuild cost

- Skipping flood or earthquake coverage because “it won’t happen here”

- Forgetting to update the policy after a renovation or big purchase

- Choosing depreciated payouts (actual cash value) over replacement cost

- Setting liability too low when a quick fix is cheap and easy

How to Lower Your Premium Without Gutting Your Coverage

Cutting your bill doesn’t have to mean cutting your protection. There’s a smart way to do both.

Start with discounts, because insurers offer more than they advertise. Bundling your home and auto policies alone can save you around $1,000 a year with some companies.

A few more ways to trim the cost safely:

- Install security systems and smart leak detectors

- Upgrade an old roof, plumbing, or electrical system

- Keep a claims-free record when you can

- Raise your deductible, but only to an amount you can comfortably afford

- Ask about loyalty, new-customer, and safety discounts

- Review your policy yearly and re-shop every couple of years

And here’s a tip people sleep on: if you want serious liability protection, a $1 million umbrella policy often costs just $200 to $300 a year. That’s a lot of peace of mind for the price.

Frequently Asked Questions

Do I legally need home insurance?

There’s no law forcing it, but if you have a mortgage, your lender almost certainly requires it. Even after you pay off the home, dropping coverage leaves you fully exposed to a six-figure loss.

What’s the difference between replacement cost and actual cash value?

Replacement cost pays to replace items at today’s prices. Actual cash value subtracts depreciation, so an older roof or TV pays out far less. Replacement cost is usually worth the slightly higher premium.

Should I file every claim?

Not necessarily. Claims can stay on your record for up to seven years and may raise your rates, so for small losses near your deductible, it’s often smarter to pay out of pocket.

Does my policy cover a home-based business?

Usually only in a limited way, with low caps on business property and liability. If you run a real business from home, ask about an endorsement or a separate policy.

How much liability coverage is enough?

Many experts suggest coverage equal to one or two times your net worth. If that feels like a lot, an umbrella policy is a cheap way to bridge the gap.

Socho, saalon ki mehnat ke baad finally aapne apna ghar khareed liya. Chaabi haath mein aati hai aur ek alag hi sukoon milta hai. Lekin ek raat tej baarish mein chhat se paani tapakne lagta hai, ya kitchen mein short circuit se aag lag jaati hai. Us waqt dimaag mein sirf ek sawaal aata hai — “Iska kharcha ab kaun bharega?”

Agar aapke paas sahi home insurance hai, toh jawab simple hai: aapki insurance company. Aur agar nahi hai, toh ye poora nuksaan seedha aapki jeb par girta hai.

Main aaj aapse bilkul wahi baat karunga jo ek samajhdaar dost karta — bina jargon ke, bina darae. Bas seedhi aur kaam ki baat, taaki aap apne ghar ke liye best home insurance aaram se chun sako.

Home Insurance Hota Kya Hai? (Aur Itna Zaroori Kyun Hai)

Simple shabdon mein, home insurance ek aisa agreement hai jisme aap har saal ek choti si raqam (premium) bharte ho, aur badle mein company aapke ghar ko hone wale bade nuksaan ka kharcha uthati hai.

Aag, chori, toofan, paani ka nuksaan, ya kisi ka aapke ghar mein gir kar chot kha jaana — ye sab cheezein aapko financially hila sakti hain. Insurance inhi anjaane jhatkon se aapko bachata hai.

Yahan ek baat yaad rakhna: ghar sirf deewaron ka naam nahi hai. Uske andar rakha saara saamaan — furniture, electronics, jewellery — ye sab bhi keemti hai. Ek achha plan in dono ko cover karta hai.

Ek Achhe Plan Mein Kya-Kya Cover Hona Chahiye?

Yahin se asli khel shuru hota hai. Har plan ek jaisa nahi hota. Best plan dhundhne se pehle, aapko pata hona chahiye ki ismein milna kya chahiye.

1. Building / Structure Cover

Ye aapke ghar ke dhaanche ko cover karta hai — deewarein, chhat, farsh. Agar aag ya bhuchaal se nuksaan hota hai, toh marammat ka kharcha yahin se aata hai.

2. Saamaan / Contents Cover

Aapka TV, fridge, laptop, furniture, jewellery — ye sab “contents” mein aate hain. Chori ya aag mein agar ye barbaad ho jayein, toh inka claim milta hai.

3. Liability Cover (Sabse Zyada Ignore Kiya Jaane Wala)

Maan lo aapke ghar aaya koi mehmaan phisal kar gir gaya aur uska haath toot gaya. Uske ilaaj ka kharcha aap par aa sakta hai. Liability cover aise legal aur medical kharchon se aapko bachata hai.

4. Additional Living Expenses

Agar aapka ghar itna kharab ho jaaye ki usme rehna hi mushkil ho, toh marammat ke dauraan hotel ya kiraye ke ghar ka kharcha ye cover deta hai. Logon ko iske baare mein tab pata chalta hai jab zaroorat padti hai — aur tab tak der ho chuki hoti hai.

Apne Liye “Best” Plan Kaise Chunein? (7 Practical Tips)

Yaad rakho — sabke liye “best” alag hota hai. Ek crore ki property wale ki zaroorat aur ek 2BHK flat wale ki zaroorat ek jaisi nahi ho sakti. Toh chaliye, step by step samajhte hain.

1. Pehle Apni Zaroorat Samjho, Phir Plan Dekho Sabse badi galti ye hoti hai ki log seedha “sabse sasta plan” dhundhte hain. Pehle baitho aur hisaab lagao — aapke ghar ki value kitni hai? Andar ka saamaan kitne ka hai? Jab number saamne hoga, tabhi sahi cover amount chun paoge.

2. Ek Nahi, Kam Se Kam 3-4 Quotes Compare Karo Pehli company jo mile, uspe haan mat bol dena. Alag-alag companies ke premium aur coverage mein zameen-aasmaan ka fark ho sakta hai. Comparison websites ya ek bharose wale agent se options leke compare karo.

3. Fine Print Aur “Exclusions” Zaroor Padho Ye sabse boring lagta hai, lekin yahi sabse important hai. Har policy mein kuch cheezein hoti hain jo cover nahi hoti (inhe exclusions kehte hain). Jaise — kai policies mein puraani wiring se lagi aag cover nahi hoti. Claim ke waqt ye baatein bada jhatka de sakti hain.

4. Deductible Ka Sahi Balance Rakho Deductible wo amount hai jo claim ke waqt aapko apni jeb se bharna padta hai. Zyada deductible matlab kam premium, lekin claim ke waqt jeb zyada dheeli. Aisa deductible chuno jo aap aaram se afford kar sako.

5. Company ka Claim Settlement Record Dekho Sasta premium tab tak bekaar hai jab tak company time par claim na de. Online reviews padho, doston se poocho. Jo company “easily claim deti hai”, wo thode mehnge premium ke bawajood behtar deal hai.

6. Discounts Aur Bundling ka Faayda Uthao Bahut log nahi jaante ki insurance par discount bhi milta hai. Ghar mein fire alarm, security camera, ya achhe locks lagwane par premium kam ho sakta hai. Kai baar do policies (jaise home + car) saath lene par bhi achha discount milta hai.

7. Har Saal Apni Policy Review Karo Aaj jo plan perfect hai, wo 3 saal baad shayad chhota pad jaaye. Agar aapne ghar renovate karaya ya koi mehnga saamaan khareeda, toh apna cover bhi update karwao.

Ek Choti Si Kahaani (Jo Aapki Aankhein Khol Degi)

Meri jaan-pehchaan mein ek sahab the. Unhone sabse sasta home insurance liya, ye soch kar “chalo paise bach gaye.” Premium kam tha, sab khush.

Phir ek monsoon mein unke ghar mein paani bhar gaya aur mehnga furniture barbaad ho gaya. Claim karne gaye toh pata chala ki unki “basic” policy mein paani ka nuksaan cover hi nahi tha.

Jo paisa unhone premium par “bachaya” tha, uska kai guna nuksaan ek hi din mein ho gaya. Sabak simple hai — sasta hamesha achha nahi hota. Sahi cover, sahi keemat par lena hi asli bachat hai.

Plan Khareedne Se Pehle Ye Checklist Zaroor Dekho

- Kya structure aur contents dono cover ho rahe hain?

- Kya flood, earthquake, fire aur theft jaise zaroori risks shaamil hain?

- Exclusions (jo cover nahi hai) kya hain — clearly padha kya?

- Deductible kitna hai, aur kya aap use afford kar sakte ho?

- Company ka claim settlement record kaisa hai?

- Koi discount ya bundle option available hai kya?

Agar in sab ka jawab “haan” mein hai, toh samajh lo aap sahi raaste par ho.

Aakhri Baat

Apna ghar shayad aapki zindagi ka sabse bada investment hai. Use kisi anjaane haadse ke bharose chhod dena samajhdaari nahi hai.

Best home insurance wo nahi hai jo sabse sasta ho, balki wo hai jo sahi waqt par aapka saath de. Thodi research karo, sawaal poocho, aur compare karke chuno. Yakeen maano, ek baar ki ye mehnat aage chalkar bahut bade tension se bacha legi.

Toh aaj hi baitho, apni zaroorat ek kaagaz par likho, aur 2-3 plans compare karna shuru karo. Aapka future self aapko zaroor thank-you bolega. 🙂